Setting up a limited company in the UK

This article describes thoroughly setting up a limited company in the UK. We have combined information from various sources to make it as informative as possible. Please find the necessary topics in the table of contents. By clicking on a topic, you will be taken to it directly. Next to each topic, you will also find a link to the Companies House (CH), the most reliable source, to learn more about that topic.

We strongly recommend going through all the steps and reading about different aspects of setting up a limited company. It is not necessarily the most interesting reading when you are eager to start your own business, but it will avoid problems in the future.

Check if a limited company is right for you

Limited company:

- is legally separate from the people who run it

- has separate finances from personal ones

- has shares and shareholders

- can keep any profits it makes after paying tax

A Limited company is a legal person on its own. The only responsibility that the owners of the limited company have is the debt up to the value of their initial investment.

The main disadvantages of registering a limited company are that you must also register with HMRC for corporation tax, most of your company’s information is public, People with Significant Control (PSCs) must provide a service address, accounting is more difficult, and you can only remove money if you have enough profit left after the deduction of tax and other expenses before doing so. You must follow strict procedures to remove money and pay yourself.

Choose a name

Your company’s name has to be original and not similar to some other name already registered in the Companies House, and your name must end in ‘Limited’ or ‘Ltd.’

Directors

The director of a limited company has to follow the company’s rules, shown in its articles of association, keep company records and report changes, file his accounts and Company Tax returns, tell other shareholders if you might personally benefit from a transaction the company makes, and pay Corporation Tax.

Shareholders

Shareholders are the organisation’s proprietors and have certain rights, such as the capacity to make changes. You can be a director and a shareholder at the same time. A limited company must have at least one shareholder who will become a director.

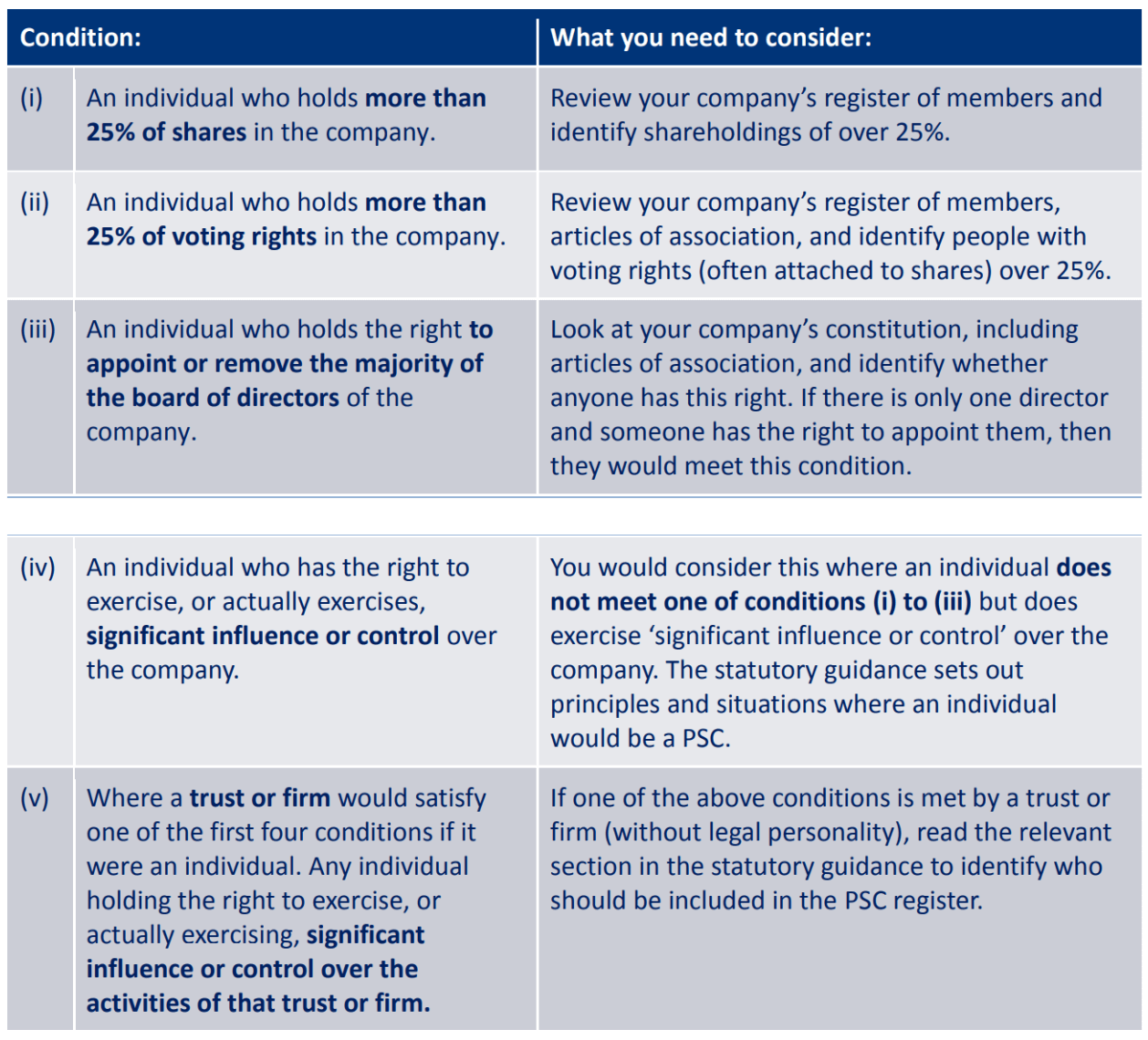

Identify people with significant control (PSC) over your company

Individuals who possess or control organisations are required to be recognised in the UK. The company  must file the PSC information with the central public register at Companies House. The PSC register helps increase transparency over who owns and controls UK companies and will help inform investors when they consider investing in a company.

must file the PSC information with the central public register at Companies House. The PSC register helps increase transparency over who owns and controls UK companies and will help inform investors when they consider investing in a company.

An officer of the company is required to:

- Identify the people with significant control (PSCs) over the company and confirm their information

- Record the details of the PSC on the company’s own PSC register within 14 days. Provide this information to Companies House within a further 14 days.

- Update the information on the company’s PSC register when it changes within 14 days.

- Update the information at Companies House within a further 14 days

- Confirm to Companies House that information on the public register is accurate, where it has not been updated in the previous 12 months.

Prepare documents agreeing on how to manage the company

Every limited company needs these two documents:

Memorandum of association – a legal statement signed by all initial shareholders or guarantors agreeing to form the company

Articles of association – written rules about running the company agreed upon by the shareholders or guarantors, directors, and the company secretary.

Records you have to keep

You will have to keep all the financial and legal records. These include records of:

- directors, shareholders, and company secretaries

- the results of any shareholder votes and resolutions

- promises for the company to repay loans at a specific date in the future (‘debentures’) and to who they must be paid back to

- promises the company makes payments if something goes wrong and it’s the company’s fault (‘indemnities’)

- transactions when someone buys shares in the company

- loans or mortgages secured against the company’s assets

Register your company

Start your application HERE in Companies House.

Open a bank account

If you have a limited company trading in the UK, you must have a UK bank account under the law. Let’s dive into more details on opening a UK business bank account. Read more from our other blog post: How to Open a Business Bank Account in the UK.

If you have a limited company trading in the UK, you must have a UK bank account under the law. Let’s dive into more details on opening a UK business bank account. Read more from our other blog post: How to Open a Business Bank Account in the UK.

VAT

As an owner of a limited company, there’s no guarantee that you’ll be familiar with every tax obligation. In simple terms, Value Added Tax is that extra fee that tops the price of services, goods, and invoices. Most companies are not immediately registered for VAT after making it to the books. Moreover, these companies don’t need to pay or register for VAT, except if their annual returns surpass a certain figure.

That said, the VAT Flat Rate Scheme (FRS) was created for smaller establishments with an annual turnover of about £150,000. What’s the need? The thing is, the scheme allows this company to pay HMRC a flat percentage of their sales. However, this depends on the company’s industry and usually amounts to less than the regular VAT rate. Regardless, it allows small companies to charge clients at 20%.

As an incentive to attract companies to register for the flat rate, owners will enjoy a 1% discount on VAT in the first year. Moreover, you must pay HMRC a percent of your turnover instead of paying out the VAT on every purchase. Your company can take up what’s left when you make a difference. This happens when you come to balance your VAT.

When registering for the VAT Flat Rate Scheme, consider whether your business clients are also registered for VAT. You have to ensure that the additional fee they are paying doesn’t have a punishing impact on their finances. You don’t want to start losing your clients.

To calculate what you give to HMRC regarding your return, deduct the VAT you pay on your expenses from the one you charge on invoices. The difference sums up what you owe.

Corporation tax

Besides the VAT, you need to register your limited liability company for Corporation Tax. Corporation tax is added to your company’s gains immediately after you pay your employees’ salaries. This addition comes up before you can withdraw dividends as a major shareholder.

All limited liability companies must submit CT600 yearly and are obliged to pay tax on their profits. Significantly, the first tax return after establishing your company should be filed within 12 months of your company’s first year. Moreover, payment should be made within nine months plus one day at the end of your company’s year.

We advise you to sort out your tax business sooner rather than position it. Be sure to submit the form on time. Please note, however, that these are merely the main taxes you will be obligated to; you may be subject to paying other taxes.

Personal income tax

Your company will pay its corporation tax. But that is not where it ends for tax. You are liable to pay tax on the income you earn. Income usually comes in the form of salary and dividends from your company.

When completing your company’s return online, you must complete a Self Assessment by 31 January following your tax year. When posting your Self Assessment, you must submit it by 31 October, the exact year of the tax year.

Be sure to register with HMRC and inform them that you have to pay personal tax. It’s quite easy to do so. You can pay for their website.

Employers Liability Insurance

If you employ people in your limited company, you must pay the employer’s liability insurance. This insurance protects company owners against claims brought by an employee for injury and other unforeseen events. However, if you’re the company’s only employee and possess over 50% of the shares, you are not obligated to have this insurance cover.

Public Liability

Public liability seeks to insure you against damage or death to a third party and their property when your actions lead to the event. Although you’re not under any compulsion to opt for public liability, you must safeguard anyone who is affected via your services.

Professional Indemnity

This covers you against claims made against your profession or work, especially as a result of your negligence.

Moreover, it’s best you also consider Tax Investigation Insurance. It is insurance against the finances incurred during a potential investigation by HMRC into your limited company. This insurance is important because the investigation wastes time and money.

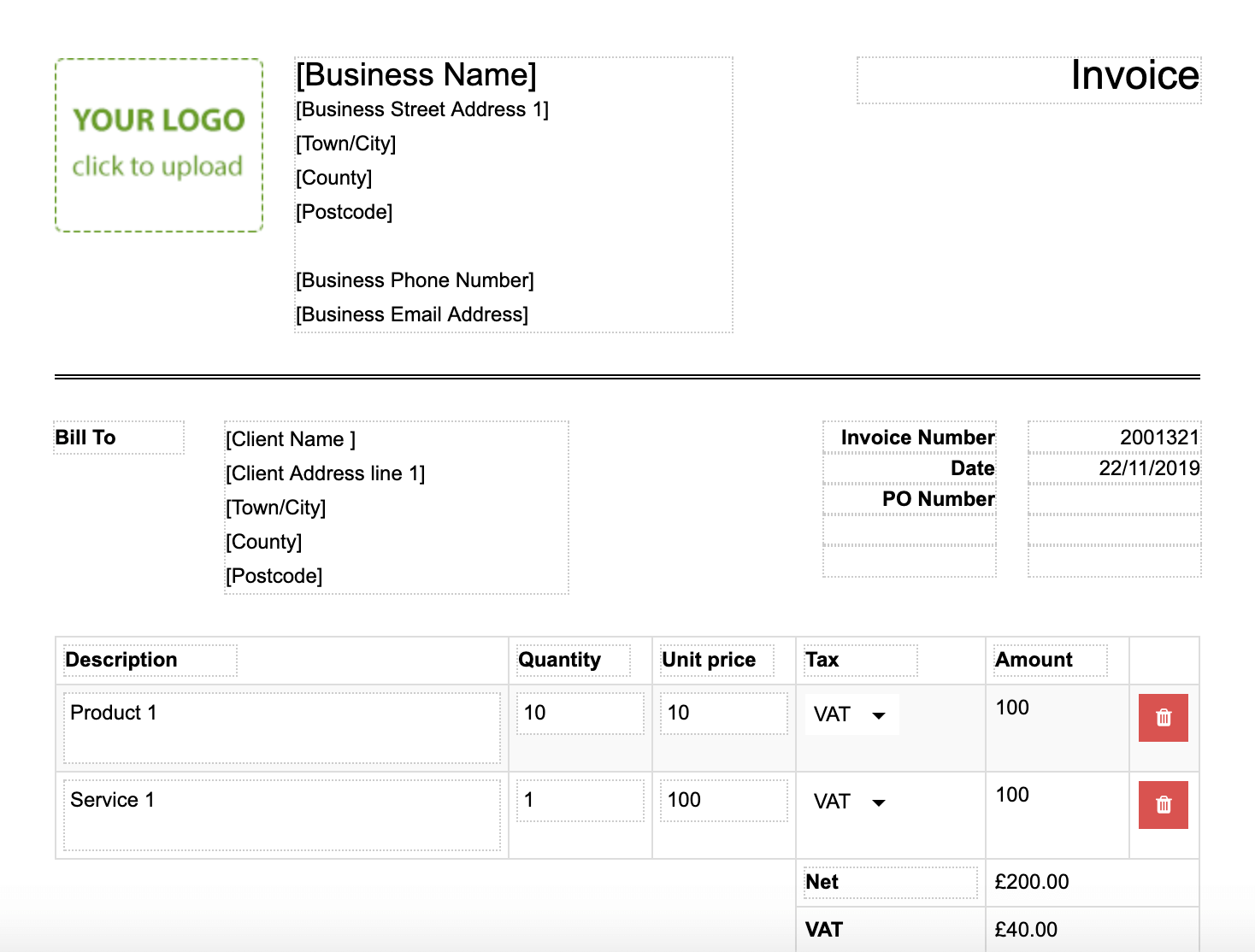

Invoicing

To accept payment for your company’s services, you should raise an invoice and issue it to your clients.

Now, there are some legal guidelines you have to follow when making an invoice. Numerous requirements should be present to validate the invoice. Significantly, it should possess the word ‘invoice’ and the following:

- The invoice number. If you’ve registered for VAT, this number must be in sequence and should begin with the number next to the one that ended the last invoice.

- Name of company, business address, and registration number (appears on the Certificate of Incorporation you were issued).

- Client’s name/address.

- A detailed description of the goods or services provided.

- The date or time of supply (the tax point) differs from the date on the invoice.

- Supply an itemised description that shows the unit price before and after VAT. Also, show the rate of VAT, the amount payable, and the final VAT charged.

- Include the payment terms. This helps your client know when the payment is for and informs them how to make it. To achieve this, we created some invoice templates that have all the information fields you need. Click here to download without cost.

Expenses

Please note that expenses must be ‘wholly and exclusively’ used for business. You can hit the rocky paths when you begin to spend personal expenses for the business. The cumulative cost of your expenses is usually removed from the revenue which you can be taxed from. For instance, if your profit is £10,000 and your business expenses are worth £1,500, you are only obligated to pay £8,500 as the corporation tax of your company’s revenue.

Kindly note that this is merely an isolated tax example to show how expenses determine your tax fee. Your tax bill will give room to VAT flat rate, PAYE salaries, and income thresholds.

Any expense that functions for two purposes will not be accepted because it’s not solely for business use. So, buying a suit for work, which you will likely use personally, will not work in this case, but purchasing a specialised outfit needed on a building site is.

However, you can claim personal expenses for business needs incurred before or during the establishment of your limited company.

Salary & dividends

Your business profits are solely the property of your limited company. If you want to withdraw an income from the firm, you must go through either dividend if you own the company or a salary if you’re an employee.

While functioning as both an owner (or shareholder) and employee (director) of the limited company, you can build the most tax-efficient way to get an income. You can split your payments between dividends and salary by doing the following:

If your company falls out of the IR35 legislation, you can earn a salary at either the level below the Tax-free thresholds and NIC or in line with the American minimum wage.

Have it at the back of your mind that the national minimum wage does not necessarily apply to companies that do not have a contract with their employees. This will be the case for one-man companies. Note that the most tax-efficient allowance or salary you can pay depends on the tax year. The reason is that income and NIC tax bands fluctuate yearly because of inflation.

Dividends signify the money you can withdraw from the after-tax profits of the limited company as a shareholder. Ensure that your company has available profits that can let you withdraw dividends. If not, the money paid would be named as the director’s loan.

Although dividends bypass National Insurance taxes, they are prone to Corporation Tax. Moreover, until your salary or income scales over the higher rate tax threshold, dividends will be taxed much lower. However, the tax controllers know that it would be unfair to tax this income twice, so do well to claim a tax credit on this amount. You can utilise our Personal Tax Estimator to discover the most tax-efficient combination of dividend and salary.

PAYE/National Insurance

To pay salaries, you must create a Pay As You Earn (PAYE) scheme with HM Revenue & Customs (HMRC). You also need to take out all National Insurance liabilities. Failure to do this properly within the given time can incur financial penalties.

What is PAYE? it’s a compulsory means of taxation where you must remove an amount from staff salaries. PAYE is applied to those earning an annual salary over the Employee National Insurance Threshold. You need to notify the HMRC whenever you pay an employee. The process will be handled by Crunch software which complies with RTI.

For further details and inquiries on RTI, visit HMRC’s website. The salary you must pay largely depends on you, but you must consider the tax benefits of paying under the minimum thresholds for taxable dividends and salaries.

IR35

IR35 legislation is a barrier that helps prevent permanent employees from disguising themselves as limited companies or self-employed to enjoy lower tax benefits.

Although this legislation confuses people, it is straightforward to use. It determines if you are employed or retain your role as a contractor while you provide your services to your client.

IR35 examines how much involvement a client has in operating your company and how much regulation surrounds your work. You are the sole authority in your limited company, and the way you work should be answerable to you.

Summary

Setting up a limited company in the UK is not hard. It is rather convenient and fast if you have done your research and are the only owner and director of the company simultaneously. Yes, it is a bit more complicated if you have multiple shareholders and you need to decide your roles in the company, but still, you can do it!